Updated on

The Rise of the 3rd Force in Retail: Social Commerce

There has been a lot of discussion and even hype around the dramatic rise of “social commerce”, especially in the last 12 months. While the COVID-19 pandemic has of course given a major boost to ecommerce spurred by lengthy lockdown-like situations and restricted mobility globally, social commerce has seen even faster growth in recent times. Clearly social commerce is a fast-rising third force in retail, after ecommerce and traditional brick-and-mortar retail.

What is Social Commerce?

Social commerce refers to the integration of ecommerce with social media. It is about buying and selling through social media platforms, which include primarily social platforms such as Facebook, Instagram, WeChat or WhatsApp, as well as dedicated social commerce platforms such as Pinduoduo and Yunji (China) or Meesho and Bulbul (India). Essentially social commerce cuts multiple stages with an online purchase journey and enables sellers to sell products directly through social media networks:

Figure 1: Social Commerce Value Chain

Figure 2: Building Blocks of Social Commerce

The social commerce ecosystem is enabled by rapid advances in the smartphone ecosystem and digital payment infrastructure. Figure 2 shows the various building blocks that come together to create an ecosystem for social commerce.

How big is Social Commerce?

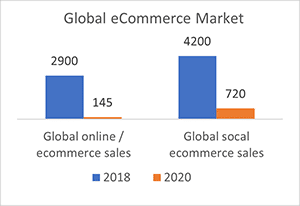

There are various and wildly varying estimates of the global social commerce market, and perhaps the market is evolving so rapidly that it is too early to come out with exact numbers and forecasts. The GSM Associations report on Social Commerce published in December 2019 projects the global social commerce market at $720 billion in 2020.

Globally, China has been the leading market for Social Commerce, and it accounts for 13% to 15% of online retail sales in China, and is growing two times faster than the growth of the online retail sector.

All indications show that India will see similar growth in social commerce, which could grow rapidly to account for 15% to 20% of online retail in India in the next 10 years. This would create a market worth $70B (more than 2 times the size of the current e-commerce market in India). Another recent report quoting a Bain & Company study indicates that the Indian social commerce space is estimated at $1.5–$2 billion in gross sales in 2020, and will grow to $16–$20 billion by 2025.

What is driving the growth of social commerce?

Social commerce is not new and has been around for more than a decade. However, until recently most of the growth of social commerce was largely limited to China, where platforms such as WeChat have built up a massive ecommerce business. In the last 5 years or so, there has been definite growth in other global markets, with Facebook, Instagram and WhatsApp gaining traction as social commerce platforms.

Some of the key drivers for social commerce growth are:

For buyers

- Power of community referrals and recommendations – Customers tend to trust recommendations from friends and family who form part of their social networks

- Power of micro-influencers

- Increased trust driven by direct interaction with suppliers

- Ability to procure very niche and regional products

For Sellers

- Easier access to a large customer base

- Higher margins as they connect directly with buyers

- More control over the production-to-supply value chain with higher visibility of customer demand

- Bypasses the need for owned digital stores or relatively expensive digital marketing initiatives (especially when the approach uses social media messaging platforms)

What’s next for social commerce?

Social commerce will continue to outpace the growth of all other retail models. While the larger brands and retailers are still trying to figure out how to tap the real potential of social commerce, it is the new players and digitally native brands who are taking advantage of this platform in a big way.

In many ways social commerce has democratized the digital transformation of retail, by providing the sellers and buyers a viable third channel.

This model is far from being “stable” and it is continuously evolving, driven both by technology changes as well as other extraneous factors such as the pandemic and regulatory environment.

Those vendors who are able to quickly adapt to these changes and can come up with a sustainable and viable social commerce strategy will emerge as winners in the coming years.

Ajith Sankaran

Ajith has over 21 years of experience in analytics, market intelligence and business consulting, and manages delivery for Course5’s analytics and insights businesses leading a...Read More

Don’t miss our next article!

Sign up to get the latest perspectives on analytics, insights, and AI.